Table of Contents

I. Introduction: Navigating the Price Puzzle of Chinese Cotton Yarn

II. The Current Market Snapshot: Prices, Trends, and Pressures

III. Deconstructing the Price: A Formula for Chinese Cotton Yarn

IV. Price Analysis by Key Specifications

V. Beyond Price: Critical Market Dynamics for Strategic Sourcing

VI. Strategic Sourcing Guide for International Buyers

VII. Future Outlook: 2026 Price Trajectory and Industry Shifts

VIII. FAQ: Answering Key Questions for International Procurement

I. Introduction: Navigating the Price Puzzle of Chinese Cotton Yarn

For global procurement managers sourcing textiles, What is the price per ton of cotton yarn in China? a straightforward question like “What is the price per ton of cotton yarn in China?” rarely has a simple answer. As the world’s largest textile producer and exporter, China’s cotton yarn market is a complex ecosystem where prices are a dynamic reflection of raw material volatility, intense domestic competition, shifting global trade policies, and nuanced product specifications.

In 2025, the market has been characterized by a significant paradox: while the national yarn capacity has expanded to over 116 million spindles, downstream demand from apparel and home textiles has remained persistently weak, creating a pronounced oversupply. This fundamental imbalance has placed immense downward pressure on prices and squeezed mill profits, making strategic, informed sourcing more critical than ever. This guide moves beyond a single price quote to provide a comprehensive framework for understanding the true cost drivers, enabling you to negotiate effectively, manage risks, and secure sustainable value from the Chinese supply chain.

II. The Current Market Snapshot: Prices, Trends, and Pressures

As of late 2025 and moving into early 2026, the Chinese cotton yarn market is operating in a buyer’s market environment, but one under significant strain.

1. The Price Reality:

The benchmark 32S combed cotton yarn is a key industry reference point. According to a November 2025 survey by the China Cotton Association, the average price for domestic 32S pure cotton yarn was approximately 20,469 RMB per ton (about $2,850 USD per ton, assuming an exchange rate of 7.18 RMB/USD). This represented a year-on-year decrease of 5.9%. Data from October 2025 indicated prices in key light textile markets continued to soften, with transactions occurring at “secretly discounted” rates below official quotes.

2. The “Gold-Silver” Seasonal Demand Disappointment:

The traditional peak demand season of September and October (“Gold September, Silver October”) failed to materialize in 2025. Order volumes were significantly below expectations, characterized by small, short-term orders rather than large commitments. This lack of seasonal uplift prevented any meaningful price recovery.

3. The Triple Pressure on Suppliers:

Chinese spinning mills, especially small and medium-sized enterprises (SMEs), are grappling with a challenging trifecta:

- High and Volatile Raw Material Costs: While global cotton prices have moderated, domestic cotton costs relative to yarn selling prices have kept margins thin.

- Weak Sales and Price Insensitivity: Downstream buyers are highly price-sensitive, and yarn prices have failed to rise proportionally with any upticks in cotton costs, a phenomenon known as “poor price transmission”.

- Mounting Inventory Pressure: With sales lagging, yarn inventories have accumulated. By the end of October 2025, average yarn inventory for surveyed textile enterprises had risen to 26.1 days of production, squeezing cash flow.

III. Deconstructing the Price: A Formula for Chinese Cotton Yarn

The final USD/ton FOB China price is not arbitrary. It is built on a clear cost-plus model, understanding which is key to negotiation:

Final Yarn Price (RMB/ton) = (Cost of Cotton per ton + Spinning Cost + Profit/Loss Margin) x (1 + VAT) + Logistic Premiums

1. Cost of Cotton (The Primary Driver, ~65-75% of Cost):

This is the most volatile component. Mills primarily use Xinjiang cotton (accounting for over 84% of usage), supplemented by imported cotton (e.g., from Brazil). The price is influenced by domestic futures (Zhengzhou Commodity Exchange) and international benchmarks (like the FC Index, which was ~72.25 cents/lb in early 2026). A key metric to track is the cotton-to-yarn spread – the difference between yarn and cotton prices, representing the theoretical processing margin. This spread has been compressed, often dipping below the break-even point for many mills.

2. Spinning Cost (Fixed & Variable, ~15-25% of Cost):

This includes:

- Labor & Energy: Varies by region (lower in inland provinces like Xinjiang, higher in coastal Jiangsu/Zhejiang).

- Financing: Interest rates for working capital to purchase cotton.

- Depreciation & Maintenance: For modernized machinery.

- Auxiliary Materials: Spinning oils, packaging.

3. Profit/Loss Margin (The Squeezed Variable):

In the current oversupplied market, this is often negative or near-zero for standard yarns. Mills may operate at a loss to maintain cash flow, market share, and workforce, hoping for a market rebound.

4. Value-Added Taxes (VAT) & Logistic Premiums:

- VAT: Typically 13% for textiles in China, often refunded upon export.

- Logistics: Includes inland trucking to port, port fees, and documentation. For FOB terms, this is a smaller adder. For CIF terms, ocean freight becomes a major component.

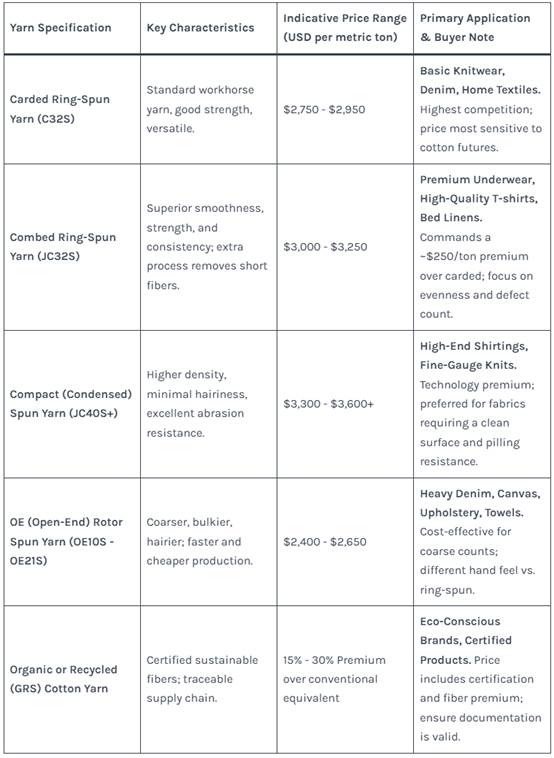

IV. Price Analysis by Key Specifications

Table: Indicative Price Range for Key Cotton Yarn Types (FOB Mainland China Port, Early 2026)

V. Beyond Price: Critical Market Dynamics for Strategic Sourcing

1. The Xinjiang Factor and Geopolitical Compliance:

Over 84% of Chinese cotton is sourced from Xinjiang. Major international buyers must navigate stringent import regulations (e.g., the U.S. UFLPA) concerning forced labor. This requires enhanced due diligence. “Non-Xinjiang” or imported cotton-blend yarns exist but carry a significant cost premium and require verifiable, transparent supply chain documentation.

2. Export Dynamics & Competitive Landscape:

Despite domestic softness, China remains a massive exporter. From January to July 2025, cotton yarn exports grew 18.27% year-on-year, indicating competitive global pricing. However, China also faces competition from lower-cost imports from Vietnam, India, and Pakistan, especially for standard counts, which caps domestic price increases.

VI. Strategic Sourcing Guide for International Buyers

- Specify with Precision: Move beyond “C32S.” Specify combed/carded, compact/conventional, evenness level, and required certifications (OEKO-TEX, GOTS, etc.).

- Request a Cost-Breakdown: Ask reputable suppliers for a basic price build-up linked to a specific cotton index (e.g., ZCE futures) to understand price adjustment mechanisms.

- Audit for Real Compliance: For sensitive markets, consider third-party audits to verify raw material origin and social compliance, not just reliance on paper certificates.

- Build Partnership, Not Just Transactions: In a distressed market, reliable mills value stable, longer-term partners. Consider volume commitments or flexible scheduling in exchange for transparency and priority during shortages.

- Factor in Total Lead Time: While production might be quick, factor in time for lab dips, sample approvals, and potential logistics delays. “Secretly discounted” prices from distressed sellers may come with higher risk.

VII. Future Outlook: 2026 Price Trajectory and Industry Shifts

The consensus for 2026 points to a continued period of weak to stable pricing with bearish risks, rather than a sharp recovery.

- Supply Side: New cotton crop expectations are for ample global supply, keeping a lid on the primary raw material cost.

- Demand Side: Recovery in global apparel consumption is expected to be slow, and destocking in Western retail channels may prolong weak order flow.

- Structural Shifts: The industry is consolidating. High-cost, inefficient capacity (often smaller, inland mills) is being squeezed out, while large, vertically integrated groups in Xinjiang and coastal hubs with better cost control and export channels are strengthening their position. The focus is shifting towards value addition—functional yarns, sustainable products, and seamless integration with fabric production—to escape the commoditized price war.

VIII. FAQ: Answering Key Questions for International Procurement

- Can I get a firm yearly price from a Chinese mill?

No. Given cotton price volatility, firm prices are typically valid for 30-60 days. Long-term agreements are often based on a floating price formula tied to a cotton index plus a fixed processing fee. - What is the realistic Minimum Order Quantity (MOQ)?

For standard yarns from a trading company, MOQs can be as low as 1-3 tons per color. Directly from a medium or large mill, MOQs typically start at 5-20 tons per specification. For custom-developed yarns, MOQs are higher. - Why do prices from different suppliers for the same “C32S” vary so much?

Differences arise from cotton origin (Xinjiang vs. imported blend), spinning technology quality (older vs. state-of-the-art machinery affecting evenness and hairiness), actual count/weight tolerance, and the financial stress level of the supplier offering “distress sale” prices. - How do I manage supply chain risks related to Xinjiang cotton?

Be proactive. Explicitly state your compliance requirements in contracts. Work with suppliers who can provide transaction-level traceability systems or are willing to spin yarn using verified imported or non-Xinjiang cotton (at a higher cost). - Are price negotiations different now than a few years ago?

Yes. The power dynamic has shifted towards buyers due to oversupply. Negotiations can more aggressively focus on cost-based pricing rather than market-based pricing. However, pushing prices below sustainable cost for mills risks supplier bankruptcy and order non-fulfillment. - What are the payment terms typically expected?

Standard terms for new relationships are 30% deposit by T/T, 70% against copy of Bill of Lading. For established relationships, terms may extend to 30 days after B/L date. Letters of Credit (L/C) are common but add cost. - Is now a good time to lock in long-term contracts?

Given the stable-to-weak price outlook for 2026, there is less urgency to lock in extremely long-term fixed prices. Consider shorter-term contracts (6-12 months) with price review clauses, allowing you to benefit from potential market softness while securing supply. - What’s the biggest hidden risk when sourcing at the lowest possible price?

The risk of quality inconsistency and financial instability of the supplier. A mill selling below cost may cut corners on raw material quality, maintenance, or labor, leading to batch variations. They are also at higher risk of ceasing operations, disrupting your supply chain.